Debt tokenization

Digitize debt instruments with transparent terms and smart repayments

Debt management often involves high costs, complex tracking, and manual operations. Brickken lets you tokenize bonds, notes, or loan claims with predefined interest and repayment terms. Our platform automates cash flows, compliance, and improves investor access.

Trusted by global innovators

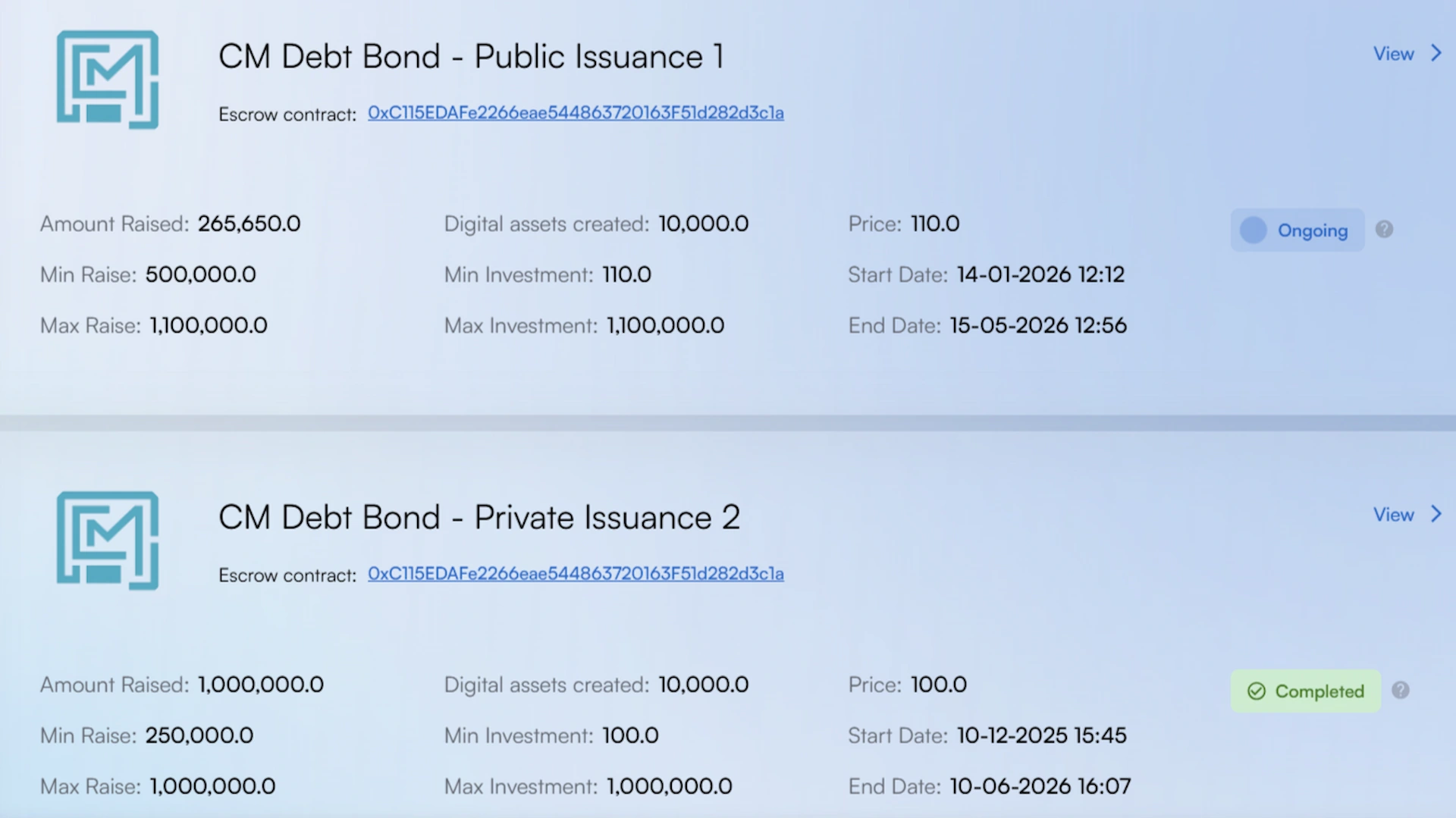

%20(1).webp)

.webp)

.webp)

What is debt tokenization?

Debt tokenization means creating blockchain-based tokens that represent regulated debt securities such as:

These tokens entitle holders to receive interest, principal repayment, or other fixed income over time.

Key benefits of tokenizing debt assets

Broader access to capital

Issuers can raise debt from global investors, both institutional and retail.

Programmable repayments

Smart contracts automate interest payments, maturity, and enforcement.

Fractional investment

Debt can be split into small-value tokens, opening access to new investor segments.

Faster settlement and lower costs

On-chain issuance removes paperwork, delays, and intermediaries.

Transparent risk and compliance

Investors can access real-time data on repayments, performance, and documentation.

Traditional vs. tokenized debt: A comparison

The Brickken platform: An end-to-end solution for digital assets management

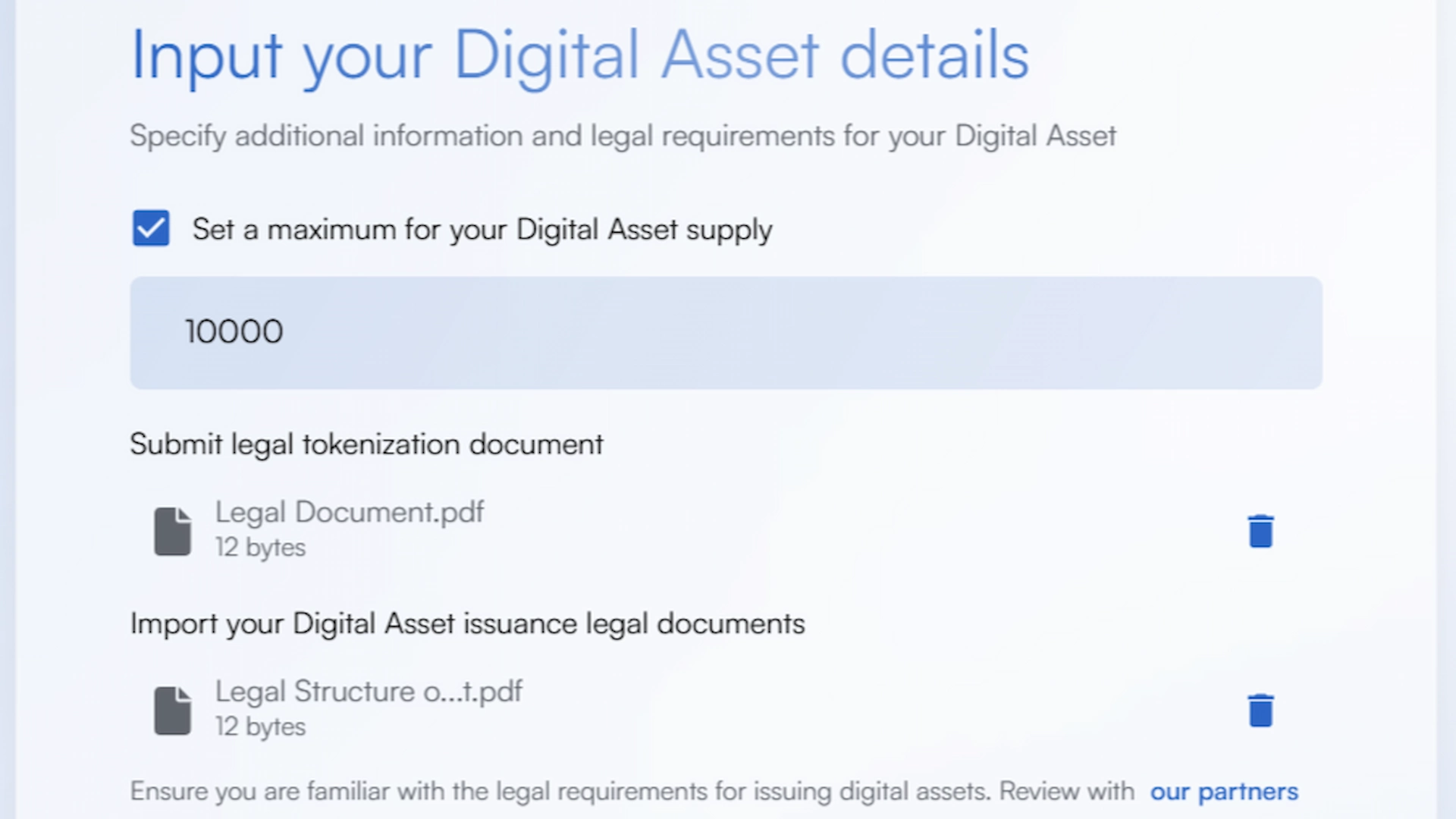

Legal structuring

Establish the legal foundation of your project. Define the structure and prepare all required documentation to ensure compliance and transparency.

Digital asset store setup

Create your investor portal the central hub where your tokenized assets will be displayed and accessed. Define your project’s identity and configure the environment investors will interact with.

Offering launch

Set the terms for your initial token offering. With the store and visuals in place, configure the funding round and get ready for investor onboarding.

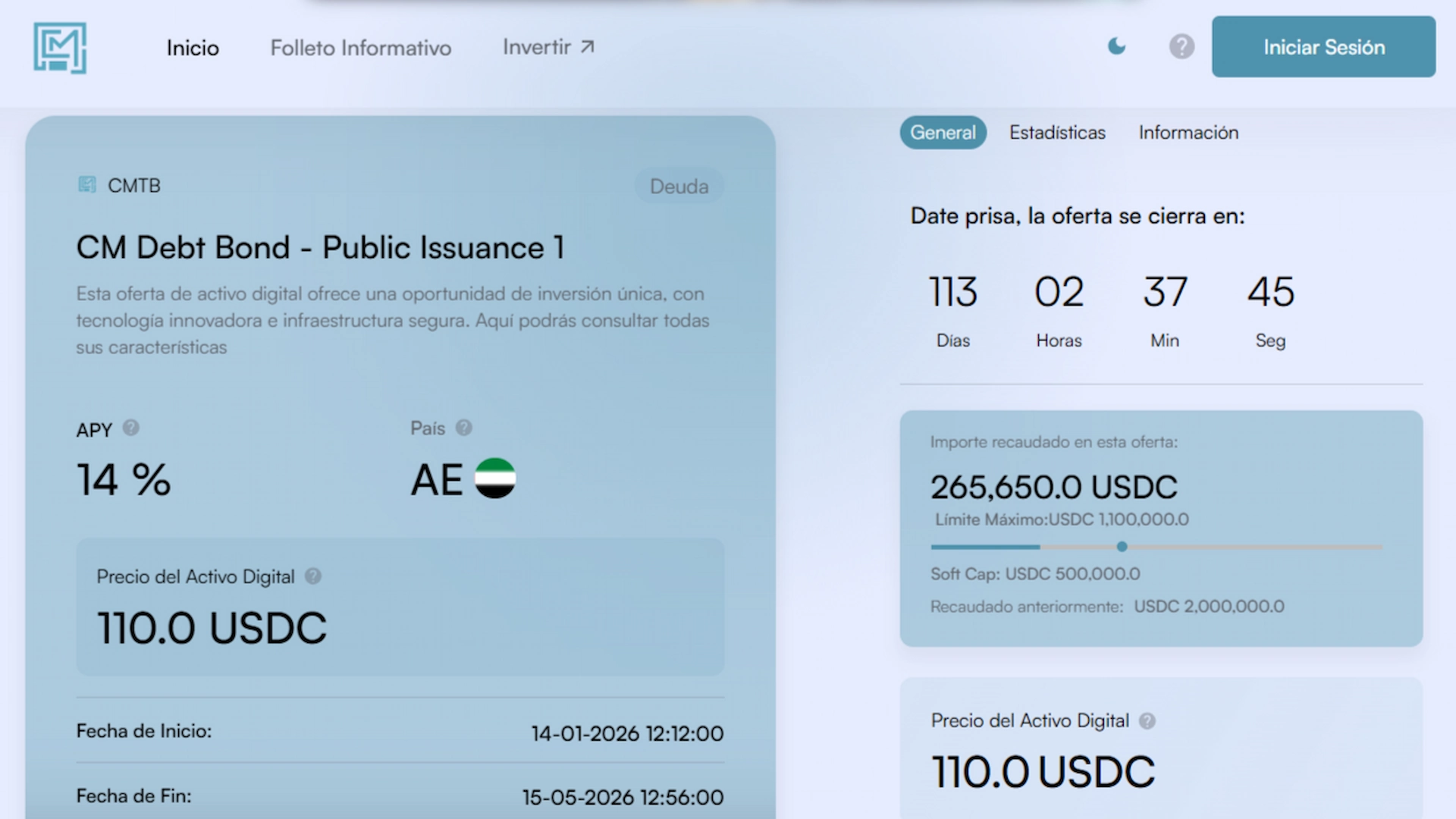

Use Cases

Deb tokenization

SME issues tokenized bond to finance growth

Example

A small manufacturer raises €500,000 through a tokenized 3-year bond.

How it works

- 5,000 tokens are issued, each worth €100.

- Token holders receive 8% annual interest.

- Repayments are executed automatically via smart contract.

Tokenization benefit

Provides SMEs with direct access to compliant debt funding.

Financing off-grid energy systems

Example

A private bank launches tokenized fixed-income products for HNW clients.

How it works

- The bank tokenizes investment-grade bonds and structured notes.

- Clients subscribe through the bank’s digital platform.

- Payouts and reporting are automated and traceable on-chain.

Tokenization benefit

Enables the bank to digitize fixed-income offerings and simplify investor servicing.

Real estate developer issues tokenized notes

Example

A property firm raises €2 million via tokenized short-term debt.

How it works

- Tokens represent loan claims backed by rental revenue.

- Investors receive 10% returns over 18 months.

- Tokens may be traded on a regulated secondary market.

Tokenization benefit

Improves project liquidity and opens access to new capital pools.

Tokenized green bond for infrastructure

Example

A clean energy company issues a €10 million tokenized green bond.

How it works

- Tokens are sold to ESG investors.

- Funds go to certified solar or wind projects.

- Returns and environmental impact reports are published on-chain.

Tokenization benefit

Links impact reporting with fixed returns in a transparent and efficient model.

Frequently asked questions

Tokenized bonds are designed for 24/7 secondary market liquidity and can be traded on regulated DLT-based trading venues or Alternative Trading Systems (ATS) among whitelisted investors.

Interest coupons and principal repayments are managed through programmable smart contracts that automatically distribute funds to verified token holders' wallets according to the predefined schedule.

Yes, debt tokens that represent a financial claim on future cash flows are generally classified as transferable securities under MiFID II and must comply with relevant securities laws.

In the event of a default, on-chain collateral management protocols or pre-defined legal wrappers (such as SPVs) trigger enforcement mechanisms to protect token holder interests and recover asset value.